Geopolitical Flashpoints and Market Stability

Saturday night’s U.S. airstrikes on Iranian nuclear facilities sent tremors through global markets, prompting a flurry of speculation around how such developments might ripple into U.S. mortgage rates. Historically, rising geopolitical tensions—especially in oil-sensitive regions—trigger a flight to safety in financial markets, pushing yields down and sometimes lowering mortgage rates. But 2025 has defied some of those norms.

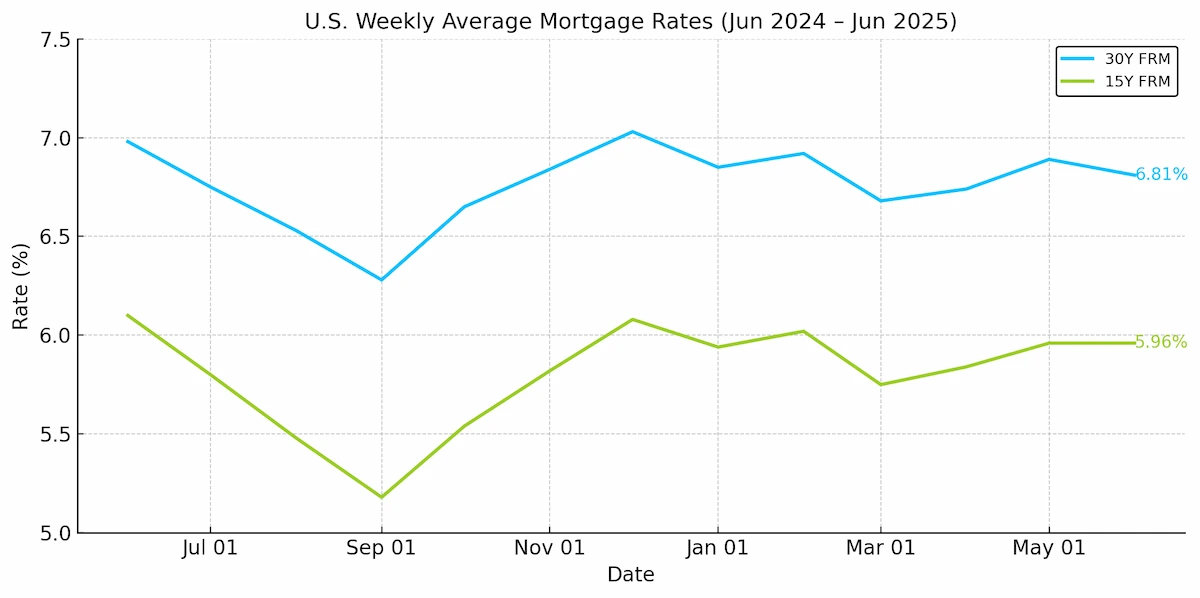

Despite headline risk, mortgage rates have remained remarkably steady. So far, this year has seen notably less rate volatility, even amid weighty catalysts ranging from central bank decisions to global conflict.

Mortgage Rates Defy the Noise

Recent events—including a Federal Reserve meeting, a dense economic data calendar, and even calls from political leaders for Fed Chair Jerome Powell’s resignation—failed to shake bond markets or move mortgage rates meaningfully.

Freddie Mac data reflects this calm. For context, forecasts for 2025 positioned the 30-year mortgage rate between 5.75% and 7.25%, with the 10-year Treasury yield ranging from 3.80% to 4.70%. To date, that outlook has largely held true.

The year’s sharpest disruption came not from war but from trade policy. When the so-called “Godzilla tariffs” were introduced, yields dropped below 4%. Although this reaction seemed exaggerated, it underscored how markets can quickly reprice risks—even when fundamentals suggest otherwise.

Improved Spreads Offer Cushion

Mortgage spreads—the difference between mortgage rates and the benchmark 10-year yield—have improved compared to the last two years. That has served as a buffer, dampening the potential for rates to spike even when Treasury yields push higher.

Yields have indeed edged toward the upper end of the forecast range, briefly topping 4.70%. But with the Fed maintaining a modestly restrictive stance and raising inflation expectations, this band remains reasonable absent any dramatic economic deterioration.

Geopolitics Break the Mold

Traditionally, Middle East conflict buoys the dollar and suppresses yields, often resulting in lower mortgage rates. Yet this year, that pattern has not held. When Israel struck Iranian targets on June 13, markets barely flinched. Even after Saturday’s U.S. airstrikes, early signs suggest muted reactions across key asset classes.

That said, Sunday night’s trading could prove more telling. Oil, dollar, and bond movements during global open hours may offer clues to how investors are recalibrating risks.

"Bond markets are less reactive this year to geopolitical shocks, which speaks to both underlying resilience and a tighter focus on domestic economic indicators." — Senior Fixed Income Analyst, Global Macro Research

Strait of Hormuz: Threat or Theater?

Iran’s vow to close the Strait of Hormuz, a chokepoint for nearly a fifth of global oil traffic, adds a layer of uncertainty. While many analysts view this as more posturing than imminent action, the threat alone is enough to keep oil traders on edge.

A sustained oil price surge could complicate central bank policy decisions, especially if it contributes to inflationary pressures. But absent a broader military escalation or genuine supply disruption, the direct impact on mortgage rates remains tenuous.

Any major fallout would likely weigh more heavily on oil-dependent economies such as China and Iran itself than on U.S. consumer borrowing costs.

What Really Moves Rates Now

Much of the speculation around mortgage rates and geopolitical risk remains hypothetical. More concrete drivers—like employment data and Federal Reserve posture—continue to hold greater sway over lending costs. Barring an unexpected economic shock, the labor market remains the more relevant barometer.

"Geopolitical noise often makes headlines, but mortgage markets still take their cues from jobs, inflation, and the Fed." — Mortgage Market Strategist, National Housing Institute

Outlook: Stability Amid the Storm

In a year filled with dramatic storylines, mortgage markets have shown surprising poise. Outside of the tariffs episode, the 10-year yield and mortgage rates have mostly respected their projected ranges.

Unless tensions in the Middle East escalate significantly—or the Fed is forced to respond to renewed inflation or labor market weakness—the trajectory for U.S. mortgage rates appears largely intact.

Investors should stay alert to headlines but keep their eyes trained on economic fundamentals. For now, steady hands appear to be winning.

Source: HousingWire, June 22, 2025.