A Counterweight to Oil Turbulence

easyJet (LON:EZJ) has weathered a volatile few weeks, with its stock price caught in the crosshairs of geopolitical unrest in the Middle East. As oil prices spiked on fears of escalation between Iran and Israel, investors punished the airline’s shares, highlighting its sensitivity to fuel costs — which account for nearly 30% of its EBITDA expenses.

Still, those fears may be overblown. Crude oil has already fallen back to $68 per barrel — near pre-conflict levels — after the U.S. launched Operation Midnight Hammer on Iranian nuclear sites, sparking but not sustaining a major supply disruption. Speculative projections from JPMorgan suggesting prices could surge to $130/bbl have so far failed to materialize.

Moreover, Iran’s attempt to leverage the Strait of Hormuz — a chokepoint for 20% of global oil flows — remains largely rhetorical. The country’s national security council has yet to approve parliamentary calls for a closure, given Iran relies on the strait for 90% of its oil exports and over 75% of state revenues.

Hedged for Headwinds

Even in a higher oil environment, easyJet appears well fortified. The company has hedged 83% of its H2 fuel at $750/MT — slightly above the current spot of $714 — and locked in 45% of its FY26 supply at an even lower average of $709/MT. This provides significant protection against price volatility and helps anchor cost projections during peak travel periods.

Meanwhile, historical fears of geopolitical contagion dragging down travel demand have not panned out. easyJet recently reaffirmed its full-year guidance, citing forward bookings for H2 that are trending higher year-over-year, even before the crucial summer travel window fully opens.

"If not for Easter’s shift to Q3, our first-half profit before tax would have shown a material improvement year-over-year." — Kenton Jarvis, CEO, easyJet

Travel Demand Lifts Results

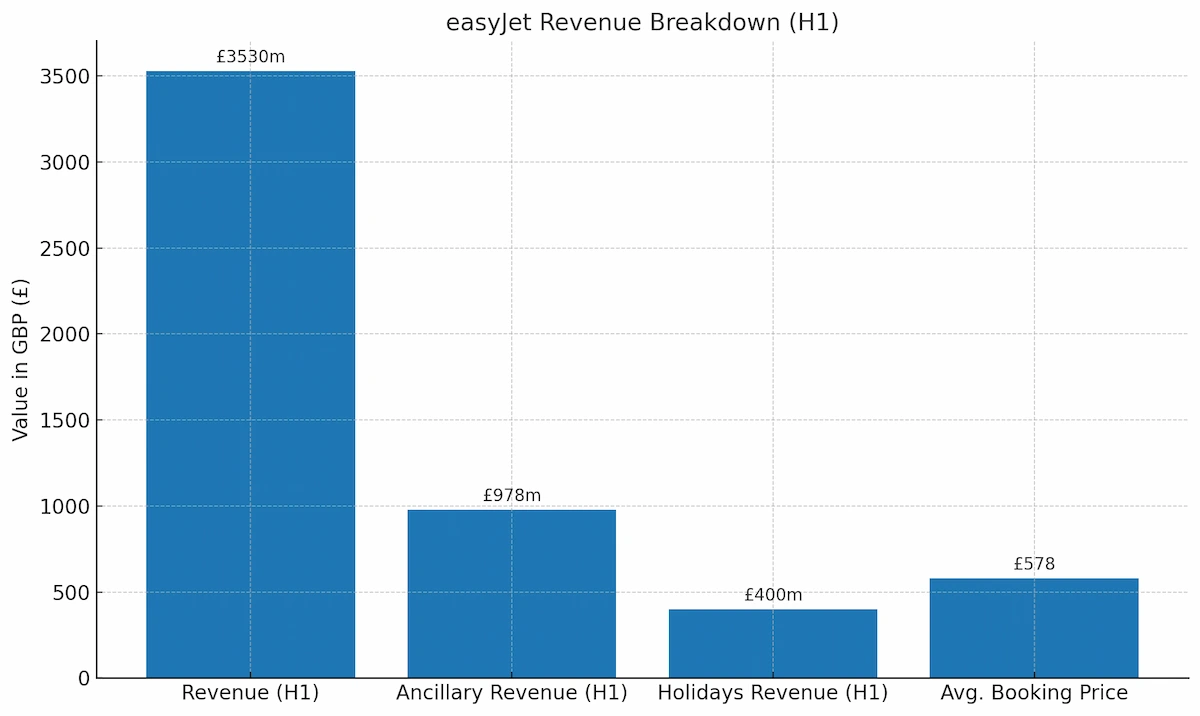

Interim figures underscore that travel appetite remains strong. In H1, group revenue rose 8.1% to £3.53 billion, led by a 5.4% jump in passenger income and a 7.6% increase in travelers to 39.37 million. Ancillary revenue also climbed 7.4% to £978 million, while easyJet’s Holidays unit stood out with a 28.6% surge in revenue to £400 million.

The company’s holiday business has now captured 9% of the market — up two percentage points — as customer numbers leapt 27.3% to 1.07 million. Average selling prices also edged higher to £578 per booking.

Critics may flag the £5 million EBITDA loss, but management attributes this primarily to seasonality and aggressive pricing on new winter routes. With Easter falling in Q3 this year, easyJet expects a rebound in second-half earnings. Adjusted for this calendar shift, PBT would have improved £50 million year-on-year.

Structural Gains in Sight

Looking beyond short-term volatility, easyJet’s strategic roadmap remains compelling. The carrier is targeting £1 billion in profit before tax over the medium term, including £250 million from its Holidays arm. Newer, more efficient aircraft are expected to deliver over £3 in unit cost savings — essential to improving margins in a competitive sector.

Route optimization efforts are also yielding dividends. The closure of 50 underperforming routes and the launch of new bases in London Southend, Milan Linate, and Rome Fiumicino are expected to boost profitability through higher utilization and improved ancillaries.

Further upside may come from increased market concentration. Wizz Air has pulled back from 14 overlapping routes this summer, creating an opportunity for easyJet to capture greater share during the critical holiday season. At the same time, with Holidays’ attachment rate still at just 6.4%, there’s ample room for cross-selling growth.

Undervalued and Underestimated?

Despite these fundamentals, easyJet’s stock has struggled to break above 600p since 2022, trading in a narrow band that fails to reflect its improving outlook. On valuation, the disconnect is striking: an EV/EBITDA of 2.7 versus a sector average of 7.7, and a PEG ratio of just 0.6 against the industry’s 1.5, point to a deeply discounted share price.

Analysts expect the airline’s EBIT margin to expand by 100 basis points to 7.41% by FY28, supported by a 16.4% CAGR in earnings over the same period. For investors willing to look past temporary geopolitical noise, easyJet may well represent one of the most attractively priced growth plays in the European airline sector.

Source: Forbes, June 26, 2025.